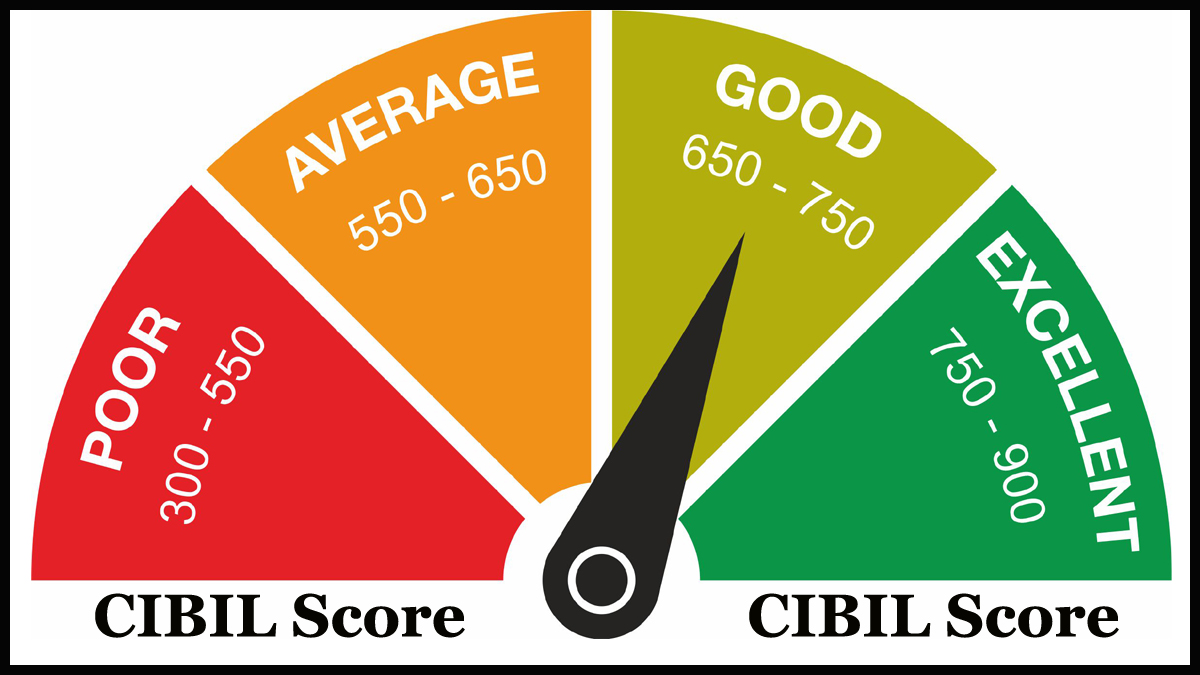

CIBIL score is a three-digit number that represents an individual’s creditworthiness. It is a numerical rating that reflects a person’s credit history and creditworthiness. The CIBIL score is calculated based on an individual’s credit report and ranges from 300 to 900. The higher the score, the better the creditworthiness.

CIBIL is one of the leading credit bureaus in India that provides credit reports and scores to financial institutions and individuals. The Credit Information Bureau (India) Limited, or CIBIL, was established in August 2000 as India’s first credit bureau. It is a repository of credit information that collects credit-related data from banks, financial institutions, and other credit grantors to create a credit report.

The credit report includes an individual’s personal information, credit history, repayment behavior, and credit utilization. It helps lenders assess the risk associated with lending money to an individual. The CIBIL score is derived from the credit report, and it indicates the likelihood of a borrower defaulting on their loan repayments.

CIBIL score is also important for individuals who are seeking loans or credit facilities. The score is also used by financial institutions to evaluate an individual’s creditworthiness and make a lending decision. A high CIBIL score indicates a low risk of default, which makes it easier for an individual to obtain a loan or credit facility.

A CIBIL score of 750 or above is considered good, and it increases the chances of obtaining a loan or credit facility. However, a score below 750 indicates a higher risk of default and reduces the chances of obtaining a loan or credit facility. In some cases, a low CIBIL score can also even lead to rejection of the loan application.

Factors that affect CIBIL score:

Credit utilization: Credit utilization is the ratio of the credit limit utilized by an individual. A high credit utilization ratio indicates that an individual is heavily dependent on credit and may have difficulty in repaying the loan. This can have a negative impact on the CIBIL score.

Payment history: Payment history is one of the most important factors that affect the CIBILscore. Late or missed payments can have a significant negative impact on the score.

Length of credit history: The length of credit history is the duration for which an individual has held credit facilities. A longer credit history indicates a better creditworthiness and can have a positive impact on the CIBIL score.

Credit mix: Credit mix is the variety of credit facilities held by an individual. A diverse credit mix, including credit cards, loans, and other credit facilities, can have a positive impact on the CIBIL score.

Credit inquiries: Credit inquiries are requests made by lenders to check an individual’s credit score. Multiple inquiries within a short period can have a negative impact on the CIBILscore.

How to improve CIBILScore:

Pay bills on time: Timely payment of bills and credit card dues is crucial to maintaining a good CIBIL score. Late or missed payments can have a negative impact on the score.

Maintain a low credit utilization ratio: It is recommended to maintain a credit utilization ratio of less than 30%. This indicates that an individual is not heavily dependent on credit and can repay the loan.

Monitor credit report: It is important to regularly check the credit report for any errors or inaccuracies. Any errors or inaccuracies should be reported and corrected.

Also Read – All about Bharatiya Janata Party

Avoid applying for multiple credit facilities: Multiple inquiries within a short period can have a negative impact on the CIBIL score. It is also recommended to avoid applying for multiple credit facilities within a short period.

Use credit facilities wisely

Use credit facilities wisely: It is important to use credit facilities wisely and not be heavily dependent on

Credit This means being mindful of spending and not using credit for unnecessary expenses. It is also recommended to pay off outstanding balances in full to avoid accumulating interest charges.

Maintain a diverse credit mix: A diverse credit mix, also including credit cards, loans, and other credit facilities, can have a positive impact on the CIBIL score. It is also important to maintain a balance between different types of credit facilities.

Close unused credit facilities: Unused credit facilities can also have a negative impact on the CIBIL score. It is recommended to close any credit facilities that are not in use to avoid accumulating unnecessary debt.

Also Read – Loan Against FD in India

Importance of CIBIL score:

The CIBIL score is an important aspect of an Individual’s financial life. It is also used by financial institutions to evaluate an individual’s Creditworthiness and make a lending decision. A high CIBILscore indicates a low risk of default, which also makes it easier for an individual to obtain a loan or credit facility. On the other hand, a low CIBIL score can lead to Rejection of the loan application or higher interest rates.

A good CIBIL score can also have other benefits. It can increase the chances of Obtaining a credit card with better benefits and rewards. It can also improve the chances of getting Approved for a rental agreement or mobile phone contract.

In conclusion, the CIBILscore is an important aspect of an Individual’s financial life. It is also used by financial Institutions to Evaluate an Individual’s Creditworthiness and make a lending decision. A high CIBIL score Indicates a low risk of default, which makes it easier for an individual to obtain a loan or credit facility. It is also important to maintain a good CIBILscore by paying bills on time, Maintaining a low credit Utilization ratio, monitoring the credit report, and using credit Facilities wisely.

Also Read – Gold loan process in India

One thought on “All about CIBIL Score”